Sustainable Finance

What is sustainability?

Sustainability focuses on meeting the needs of the present without compromising the ability of future generations to meet their needs. The concept of sustainability is composed of three pillars: economic, environmental, and social—also known informally as profits, planet, and people.

We are guided by John Elkington’s original intent behind the triple bottom line to create a business mindset that does not treat people, planet and profit as tradeoffs, rather aims to simultaneously improve our impact on all three to create more opportunity.

What is sustainable finance?

Sustainable finance refers to the process of taking environmental, social and governance (ESG) considerations into account when making investment decisions in the financial sector, leading to more long-term investments in sustainable economic activities and projects

Types of Sustainable Finance (click to expand)

Environmental, social and governance (ESG) integration is the practice of incorporating ESG information into investment decisions to help enhance risk-adjusted returns, regardless of whether a strategy has a sustainable mandate.

Socially Responsible Investing

Socially responsible investing goes one step further than ESG by actively eliminating or selecting investments according to specific ethical guidelines. The underlying motive could be religion, personal values, or political beliefs. Unlike ESG analysis which shapes valuations, SRI uses ESG factors to apply negative or positive screens on the investment universe.

Impact investments are investments made with the intention to generate positive, measurable social and environmental impact alongside a financial return. Impact investments can be made in both emerging and developed markets, and target a range of returns from below market to market rate, depending on investors’ strategic goals.

Microfinance, also called microcredit, is a type of banking service provided to unemployed or low-income individuals or groups who otherwise would have no other access to financial services.

While institutions participating in the area of microfinance most often provide lending—microloans can range from as small as $100 to as large as $25,000—many banks offer additional services such as checking and savings accounts as well as micro-insurance products, and some even provide financial and business education. The goal of microfinance is to ultimately give impoverished people an opportunity to become self-sufficient.

A bond is a fixed income instrument that represents a loan made by an investor to a borrower (typically corporate or governmental). A bond could be thought of as an I.O.U. between the lender and borrower that includes the details of the loan and its payments. Bonds are used by companies, municipalities, states, and sovereign governments to finance projects and operations. Owners of bonds are debtholders, or creditors, of the issuer.

Social Impact Bonds

A social impact bond (SIB) is a contract with the public sector or governing authority, whereby it pays for better social outcomes in certain areas and passes on the part of the savings achieved to investors.

Green/Environmental Impact Bonds

A green bond is a type of fixed-income instrument that is specifically earmarked to raise money for climate and environmental projects. These bonds are typically asset-linked and backed by the issuing entity’s balance sheet, so they usually carry the same credit rating as their issuers’ other debt obligations.

Sustainability Bonds

Sustainability bonds are issues where proceeds are used to finance or re-finance a combination of green and social projects or activities. These bonds can be issued by companies, governments and municipalities, as well as for assets and projects and should follow the Sustainability Bond Guidelines from ICMA

Development finance is the efforts of local communities to support, encourage and catalyze expansion through public and private investment in physical development, redevelopment and/or business and industry. It is the act of contributing to a project or deal that causes that project or deal to materialize in a manner that benefits the long-term health of the community.

To learn more about Impact Investing specifically, click here: https://thegiin.org

Blended Finance

(Click each heading below to expand and read the contents)

What is Blended Finance?

Bank of America Blended Finance: https://about.bankofamerica.com/en/making-an-impact/blended-finance

Watch this two-minute video explaining blended finance.

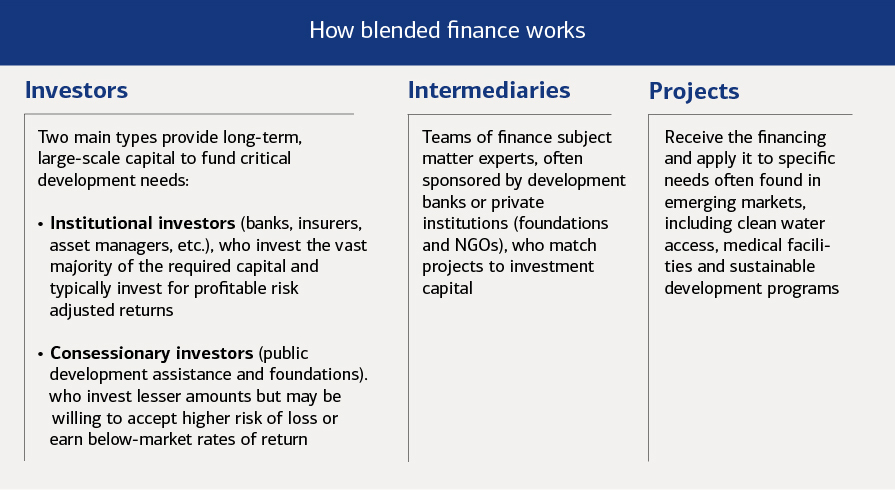

Blended finance- the use of catalytic capital from public or philanthropic sources to increase private sector investment in sustainable development

Catalytic capital is defined as debt, equity, guarantees, and other investments that accept disproportionate risk and/or concessionary returns relative to a conventional investment

*Concessionary return: Return on an investment that sacrifices some financial gain to achieve a social benefit

Institutional investors (banks, insurers, asset managers, etc.), who invest the vast majority of the required capital and typically invest for profitable risk-adjusted returns

Concessionary investors (public development assistance and foundations), who invest lesser amounts but may be willing to accept a higher risk of loss or earn below-market rates of return

- “The 2030 Agenda for Sustainable Development, adopted by all United Nations Member States in 2015, provides a shared blueprint for peace and prosperity for people and the planet, now and into the future. At its heart are the 17 Sustainable Development Goals (SDGs), which are an urgent call for action by all countries – developed and developing – in a global partnership.”

- We support the Sustainable Development Goals

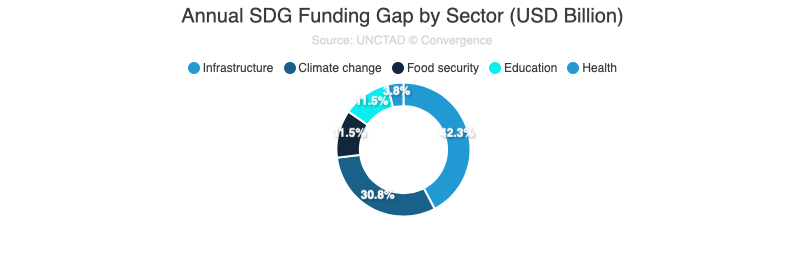

The UN estimates that the total financing needed to achieve the SDGs is nearly $4 trillion annually. Current levels of development financing are not sufficient, with an estimated $2.5 trillion funding gap per annum to realize the SDGs in developing countries alone

How does blended finance address the SDGs?

- “UN member countries reached consensus on the importance of deploying public funds to attract private investment at the Third International Conference on Financing for Development in 2015 in Addis Ababa. Convergence, along with the Sustainable Development Investment Partnership (SDIP), were established to build the blended finance market.”

Cann blended finance be used to address all of the SDGs?

- “Blended finance can only address a subset of SDG targets that are investable. For example, blended finance is highly aligned with goals such as Goal 8 (Decent Work and Economic Growth) and Goal 13 (Climate Action), while less aligned with SDGs such as Goal 16 (Peace, Justice and Strong Institutions).”

- In terms of deciding if and when to use blended finance, investors’ motivations are varied and driven by a variety of factors such as risk-return preferences, impact targets, and fiduciary responsibilities. Below are examples of situations that trigger blended finance conversations:

- An investor wants to build a certain size or type of fund but does not have sufficient capital available via conventional structuring without adjusting the risk profile of the fund.

- An investor has access to a certain amount of grant and/or public money and wants to use this funding to leverage private capital.

- An investor’s investment structure is dependent on a combination of public and private capital, e.g., a social impact bond.

- In the scenarios above, catalytic capital is utilized to address risks (perceived or real) facing market-rate investors and preventing them from entering into an investment. These risks could be associated with the piloting of a new business model or entrance into an unfamiliar market.

- Grants – public/philanthropic partner gives money to support the project that has no expectation of being repaid. These funds can be used to support non-income generating activities or early stage preparations.

- Guarantees – public/philanthropic partner offers protection (often in the form of insurance) from capital loss. (lowers the risk or increases the credit rating)

- Technical Assistance – public/philanthropic partner offers direct support to an entrepreneur, typically through a technical assistance facility or an incubator.

- Junior Equity – public/philanthropic partner buys ownership in the investment, but accepts a subordinate position in the structure, effectively accepting higher risk for lower returns. This structure is also sometimes referred to as concessional or first-loss capital.

- Flexible Debt – similar to junior equity, the public/philanthropic partner can accept subordinate terms to the debt structure, allowing for more favorable

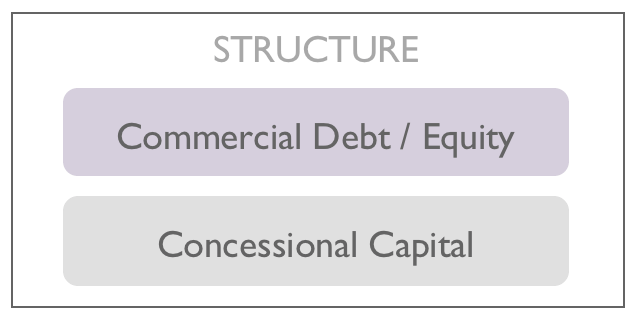

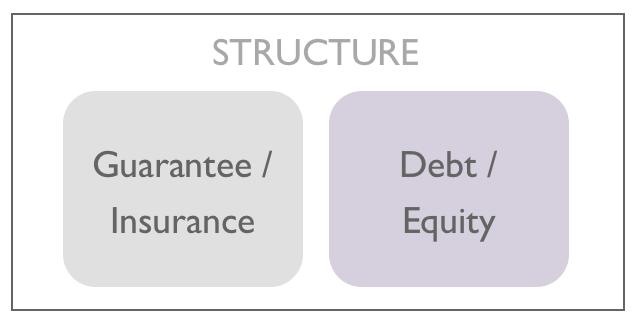

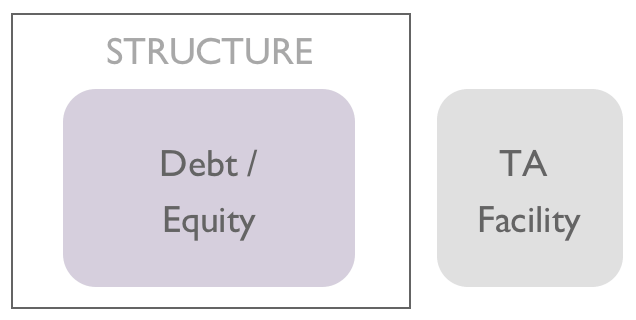

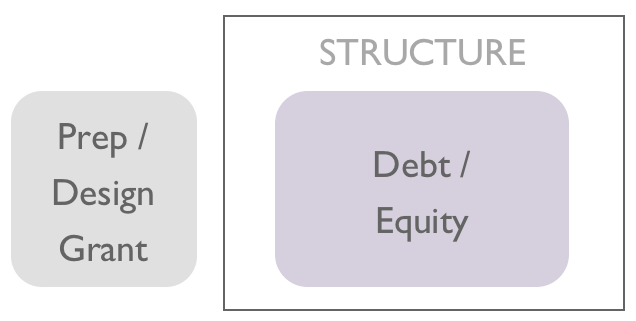

Convergence, the global network for Blended Finance, identifies four common archetypes for Blended Finance projects.

Public or philanthropic investors provide funds on below-market terms within the capital structure to lower the overall cost of capital or to provide an additional layer of protection to private investors.

Public or philanthropic investors provide credit enhancement through guarantees or insurance on below-market terms.

Transaction is associated with a grant-funded technical assistance facility that can be utilized pre- or post-investment to strengthen commercial viability and developmental .

Transaction design or preparation is grant-funded (including project preparation or design-stage grants).

Funds – Equity Funds, Debt Funds and Funds-of-funds.

Projects

Companies

Facilities

Bonds and Notes

Impact Bonds

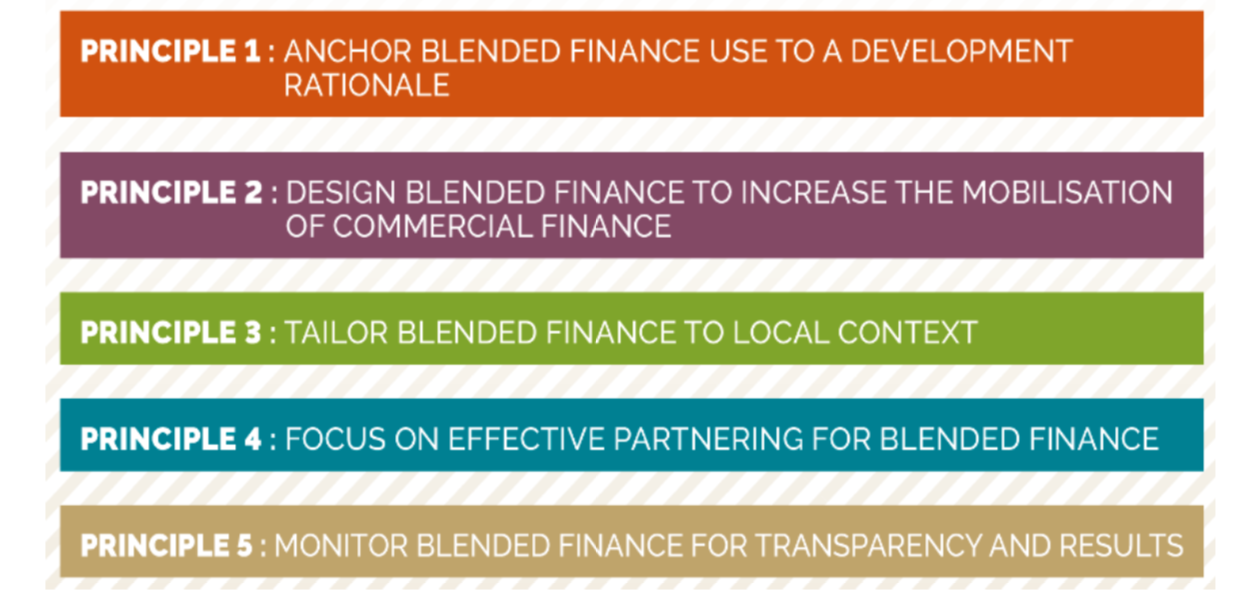

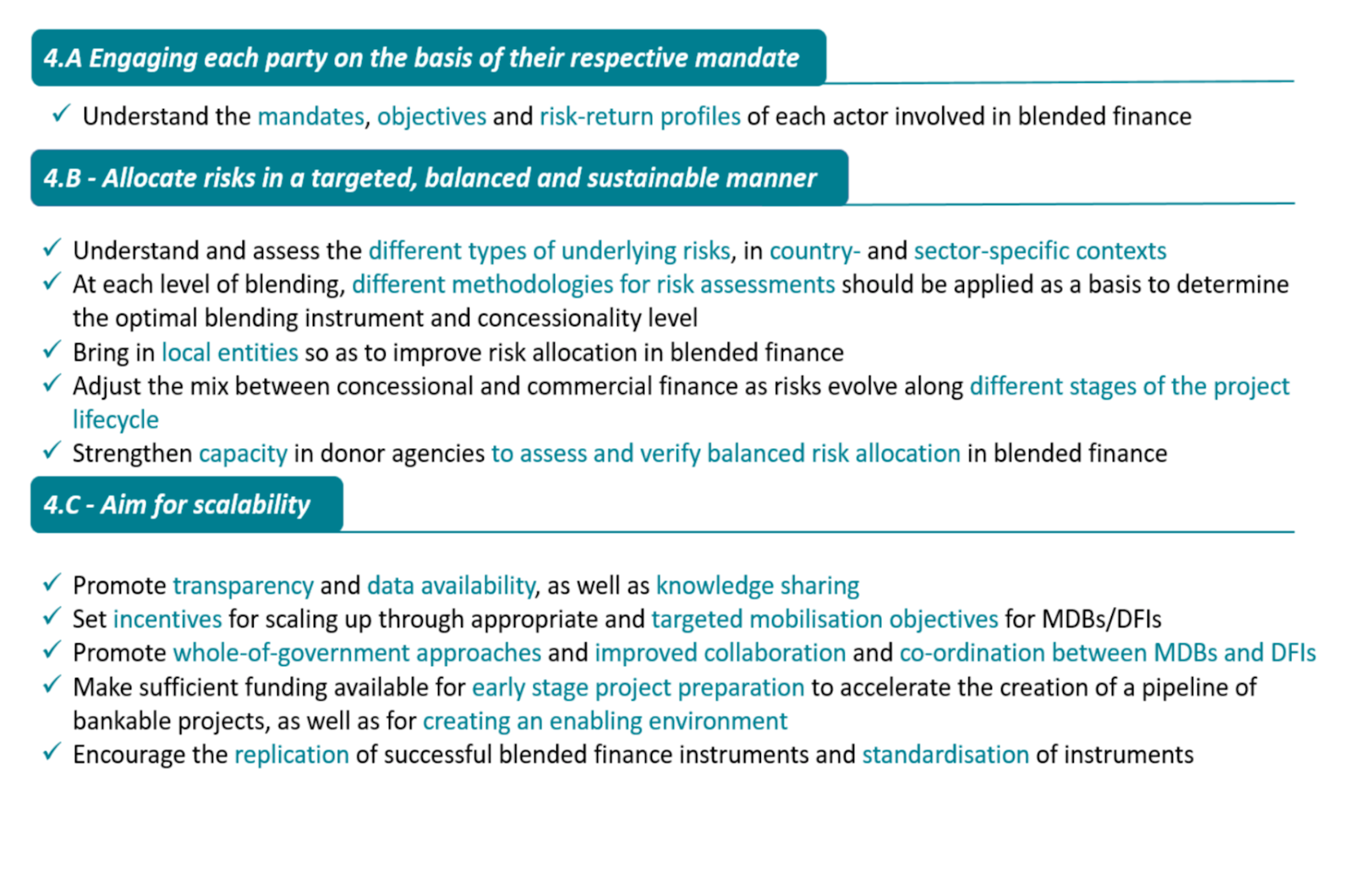

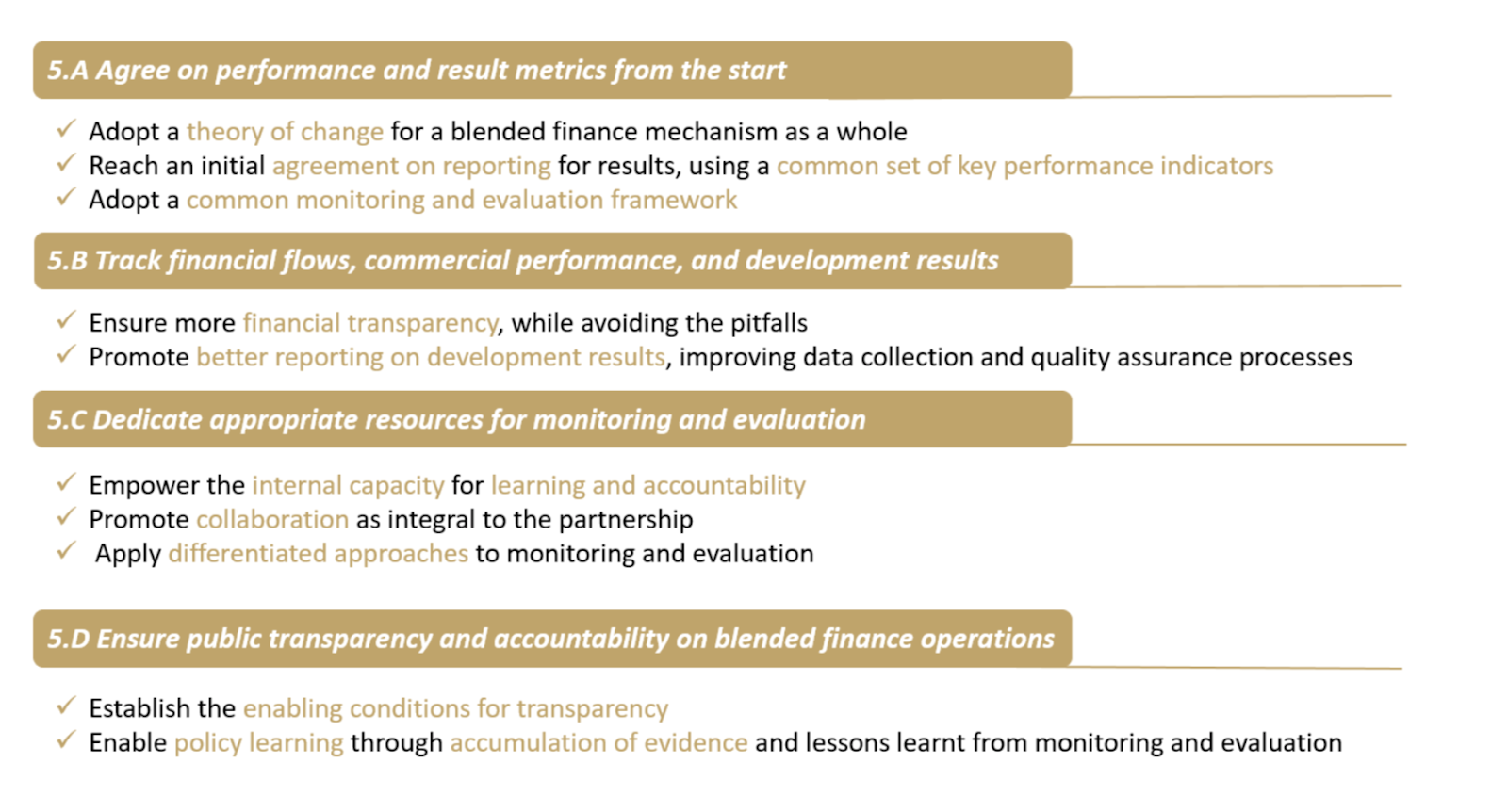

The OECD has developed 5 principles to designing a blended finance project. As explained by the OECD, “The Blended Finance Principles and the Blended Finance Guidance are effective policy tools for donor governments, development co-operation agencies, philanthropies and other stakeholders to design and implement effective and transparent blended finance programmes.” Each principal has several points and subpoints that are outlined in the following slides.

Source: https://www.convergence.finance/resource/1qEM02yBQxLftPVs4bWmMX/view

Impact investors appear in a small minority of commitments to blended finance transactions. Their commitments to blended transactions have fallen in absolute terms over time (from 137 in 2011-13 to 70 in 2017-19), and they account for a falling proportion of total commitments. Impact investors accounted for 8% of financial commitments to blended finance in 2017-19, most of which was deployed through debt (56% of their commitments compared to 44% across all years). Meanwhile, their use of equity in their commitments fell from 47% across all years, to 29% in 2017-19. Inspecting the data more closely, Convergence found that (i) only 14 impact investors deployed equity in their commitments to blended transactions in 2017-19, down from 35 in 2014-16 and 28 in 2011-13; (ii) 17 equity commitments were made by impact investors in 2017-19, down from 44 in 2014-16 and 32 in 2011-13; (iii) 22 impact investors deployed debt in 2017-19, compared to 23 in 2014-16 and 23 in 2011-13; and (iv) 33 debt commitments were made by impact investors in 2017-19, compared to 35 in 2014-16 and 30 in 2011-13. In sum, the number of debt commitments and the number of impact investors making debt commitments have been stable; however, both the number of equity commitments and the number of impact investors making equity commitments have fallen. This may reflect a movement amongst impact investors towards seniority in transactions and a reduction in their willingness to assume risk.

Impact investors represent over a fifth (21%) of active investors in blended finance (investing in three or more transactions) across all years, behind only commercial investors (28%), but their share falls to 12% when considering active investors in blended finance between 2014 and 2019. They have typically invested in smaller blended finance transactions (with a median transaction size of $50 million across all years).”

- Improving Nutrition in Rwanda

- The project consists of financing a 45,000 ton/year processing plant to produce fortified cereals to treat malnutrition in nearly one million children and pregnant and nursing women. Using maize and soy sourced and grown locally by Rwandan farmers, the processing plant develops fortified food for young children and their mothers, supporting the prevention and treatment of malnutrition among this vulnerable population. The first phase of the project costs approximately $65 million in capital expenditure and working capital. Blended finance in the subordinated debt and equity was essential to allow the project to go ahead since extensive risk factors made financing on strictly commercial terms unachievable. The risks included greenfield and market risks, fluctuations of raw material commodity prices, a lack of consistent supplies of quality maize and soy, limited access to long-term capital, and an untested private partnership model in this sector. Advisory services were also an important component in the overall structure to strengthen sourcing and build the commercial market for the products. A key lesson from the project was the early identification at the concept stage of the need for blended finance to move the transaction forward. This made it possible to create a strong partnership and align the project with the blended finance program’s objectives of supporting food security and rural incomes in a market with high risks for commercial investments. This blended finance project is supported by the Private Sector Window of the Global Agriculture and Food Security Program (GAFSP). Through the partnership, a ratio of nine was achieved on total project cost to the contribution from the donors. By supporting the local production of this fortified cereal, it is expected that the operating company will set a new standard in food production in the country and the region. It is also expected to strengthen the supply chain, as farmers learn to improve both productivity and quality of the key raw materials. The success of this public-private partnership, in which the World Food Program and the Government of Rwanda are key off-takers in the initial years, can help demonstrate a new business model for addressing key development challenges such as malnutrition. The development of a commercial market for the product will help reduce the reliance on blended finance in the future. The project provides a strong example of how blended finance can play a key role in kick-starting a new market and achieving strong long-term development impact. The success of the plant in Rwanda is expected to create a strong demonstration effect and provide a working model for other countries facing similar challenges.

- Scaling Up Solar Energy in Thailand

- An example of the role of blended finance for market creation in a more mature and higher-income situation is Thailand’s nascent solar photovoltaic (PV) power market. This market was virtually non-existent a decade ago with solar energy accounting for less than 2 megawatts (MW) of installed capacity in Thailand. Despite falling technology costs and new Thai government incentives for renewable energy developers, the market remained subdued. However, there was recognition of a substantial potential for solar energy. To leverage the government’s efforts and to support a first-mover company—Solar Power Company Group (SPCG)—to develop a utility-scale solar PV power plant in Thailand, IFC initially provided an $8 million loan from its own account. This was “blended” with $4 million in concessional financing from the Clean Technology Fund, a multi-donor fund within the Climate Investment Funds that provides middle-income countries with concessional resources for climate change mitigation projects with high impact potential. This blended finance structure enabled SPCG to mobilize enough capital from three local banks to develop two power plants with 12 MW of aggregate capacity. The early support from IFC and the Clean Technology Fund has enabled SPCG to develop nearly 300 MW of installed capacity. So far, the company’s solar farms have attracted more than $800 million in clean energy investments while avoiding over 200,000 tons of CO2 emissions annually. The success of SPCG sent positive signals to local financial markets and gave investors more confidence, providing a strong demonstration effect to markets. The overall lesson is the importance of a timely blended finance package to help secure previously unavailable long-term financing in the solar PV segment. The project illustrates how concessional donor participation can reduce risks for investors, and enable a high-impact initiative. In Thailand, investors were unfamiliar with Solar PV technology and were not convinced that the support provided by the Thai government was adequate, or would be sustained over the long term. This perception largely prevented long-term commercial capital to solar PV projects. Concessional donor participation in the project helped overcome this perception and provided enough comfort to local banks to engage in long-term financing of future projects. The case from Thailand, however, also illustrates how a blended finance solution should never be seen in isolation from regulatory reforms. In this case, a favorable regulatory regime provided the foundation for the market expansion and scale-up without further subsidies.

- Bridging the Finance Gap in Africa

- Small and medium-sized enterprises (SMEs) have traditionally been poorly served by the banking industry in Sub-Saharan Africa. Fewer than one in three medium-sized firms in the region have a bank loan or a line of credit, according to World Bank data. For small firms, it is fewer than one in five. To tackle these financial market restrictions for SMEs, IFC with support from the United Kingdom has signed a risk-sharing agreement with the European Investment Bank and Ecobank, a pan-African commercial and investment banking group. This has helped to fill the gap in financing for the enterprises operating in fragile and conflict-affected states in West and Central Africa. This risk-sharing facility has helped to overcome the challenges of lending to smaller businesses by providing access to finance to enterprises in eight African countries: Burundi, Congo, Cote d’Ivoire, the Democratic Republic of the Congo, Guinea, Mali, Chad, and Togo. A risk-sharing facility supports partner banks such as Ecobank to extend their SME lending by sharing some of the downsides if there are significant losses. The Global SME Facility, which supported the risk-sharing structure with Ecobank, operates as a comprehensive blended finance vehicle that integrates both investment and advisory services to help banks scale up SME lending and overcome market restrictions. The facility also provides the local partner, Ecobank, tools to build scale in SME lending, including advisory services and SME finance training. For Ecobank, the project helps to provide a broader customer base and, in time, stronger markets to lend to.

https://www.ifc.org/wps/wcm/connect/topics_ext_content/ifc_external_corporate_site/bf/bf-details/bf-dfi

https://www.oecd.org/dac/financing-sustainable-development/blended-finance-principles/guidance-and-principles/

https://thegiin.org/assets/upload/Blended%20Finance%20Resource%20-%20GIIN.pdf

https://www.convergence.finance/blended-finance

https://www.ifc.org/wps/wcm/connect/topics_ext_content/ifc_external_corporate_site/bf

https://www.oecd-ilibrary.org/docserver/806991a2-en.pdf?expires=1623389806&id=id&accname=guest&checksum=3D5020398CB20244F7C75D4B0D2B75EC

https://www.oecd-ilibrary.org/docserver/7c194ce5-en.pdf?expires=1623392763&id=id&accname=guest&checksum=EA5794ABF052E292DBEFBEA6C211D2A2

https://www.ifc.org/wps/wcm/connect/topics_ext_content/ifc_external_corporate_site/bf/bf-details/bf-dfi

http://www3.weforum.org/docs/WEF_How_To_Guide_Blended_Finance_report_2015.pdf

https://www.impactterms.org/blended-finance/

https://about.bankofamerica.com/en/making-an-impact/blended-finance

https://www.ifc.org/wps/wcm/connect/8e7889db-2860-4ed3-a465-54d1070ff2fb/EMCompass_Note_51-BlendedFinance_FIN+April+13.pdf?MOD=AJPERES&CVID=mbkK6Id